Here’s Why Your Wallet Is Emptying Faster This April

The Truth Behind the March 2026 CPI Surge

You are spending significantly more at the gas pump and the grocery checkout this month. Your paycheck, which felt adequate just a few months ago, is suddenly failing to stretch to the end of the week. You are not mismanaging your budget; you are caught in the crosshairs of a stubborn economic reality.

For the past year, we have been promised relief. We have all been eagerly waiting for that highly anticipated interest-rate cut to lower our suffocating credit card bills and ease mortgage rates. But the latest US core inflation March 2026 data just threw a massive, heavy wrench into those plans. The numbers are out, and they paint a frustrating picture for consumers in both the United States and the United Kingdom.

We are going to break down exactly what this new economic data means, explain why volatile energy costs are currently hijacking the global economy, and reveal how you can brace your finances for a year where rate cuts are suddenly—and painfully—off the table.

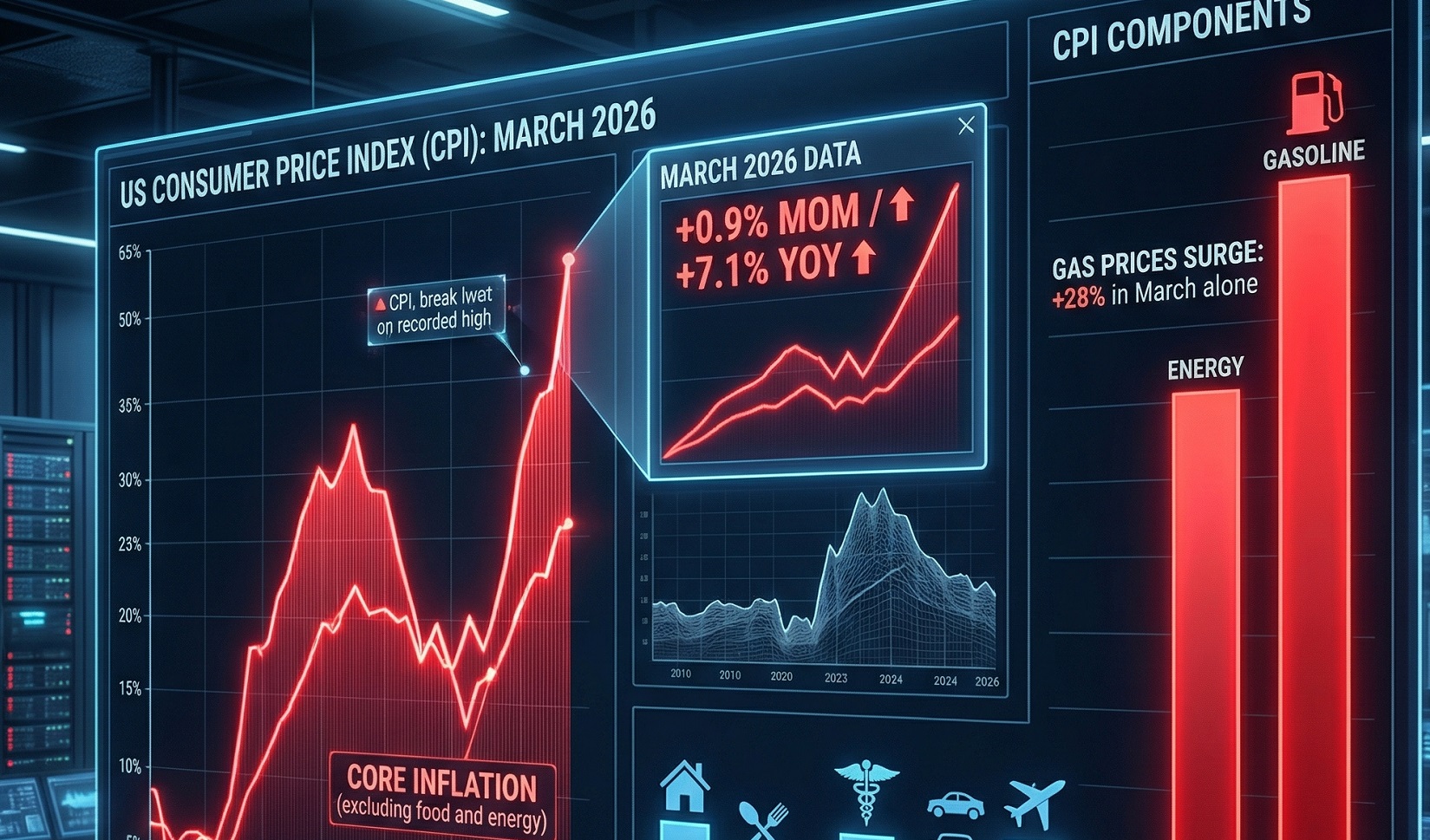

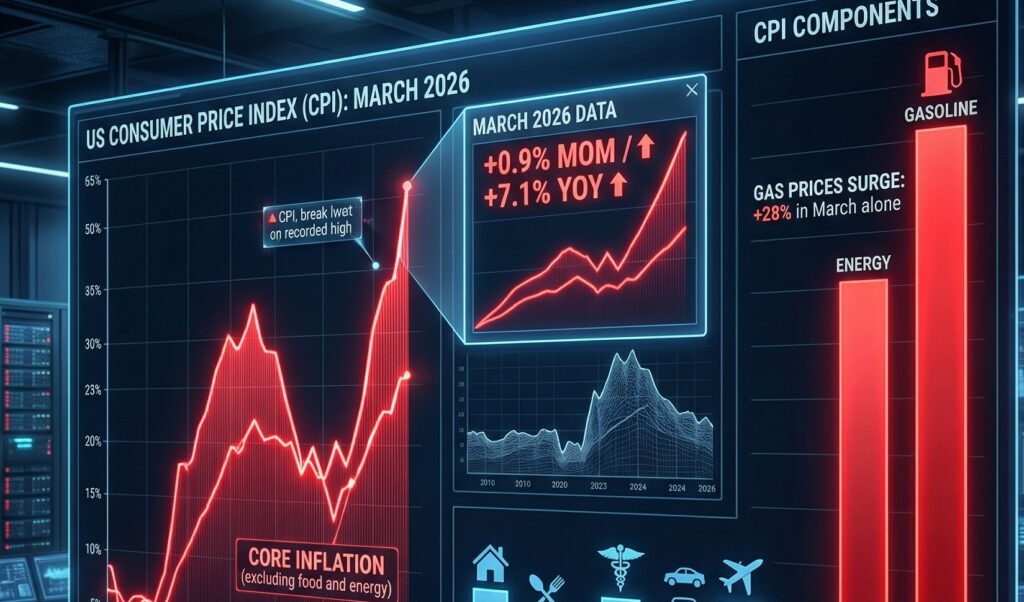

What exactly is the Consumer Price Index (CPI) telling us right now? The March 2026 CPI report reveals that headline inflation jumped to 3.3% year-over-year. This surge is aggressively driven by skyrocketing energy and gasoline costs. While policymakers focus on a lower “core” inflation rate, the actual CPI data confirms that everyday consumer prices are rising faster than expected.

The Reality of US Core Inflation March 2026 vs. Your Wallet

When the Bureau of Labor Statistics (BLS) released the March data, Wall Street had a mild panic attack. The headline Consumer Price Index (CPI) rose 3.3% year-over-year. To understand why this matters, we have to look past the percentages and look directly at your bank statement.

For the better part of late 2024 and 2025, we experienced what economists call disinflation—the rate of price increases was slowing down. Things were still expensive, but they were not getting dramatically more expensive every single month. March 2026 shattered that trend. The inflation jump we are experiencing now is highly concentrated in the things you cannot simply choose to stop buying: transportation and housing.

Shelter inflation remains historically sticky. Rents are not coming down at the pace the Federal Reserve projected. But the true culprit behind this 3.3% headline surge is energy. The cost to fuel your car and heat your home is accelerating, and it is acting as a brutal hidden tax on the working and middle class.

Pain at the Pump: Why Energy Costs and Gas Prices Are Spiking

If you live in the US, you are watching the price per gallon creep uncomfortably close to panic levels. If you are in the UK, the cost of petrol is once again dominating the morning news cycle. This is not a localized issue. It is a global supply chain bottleneck slamming directly into your daily commute.

How Global Supply Chains and Geopolitics Are Draining Your Monthly Budget

We track global commodities heavily, and the crude oil market right now is incredibly fragile. The energy costs driving the March 2026 CPI data are rooted in complex geopolitical realities.

Tensions in the Middle East have repeatedly threatened major shipping lanes over the last two years. When oil tankers are forced to reroute, the cost of freight skyrockets. Furthermore, production cuts enforced by OPEC+ have artificially constrained the global supply of crude oil just as springtime travel demand begins to ramp up in the West.

This creates a brutal domino effect. Brent crude and West Texas Intermediate (WTI) both surged in late February and March. When oil prices spike, the cost of refining that oil into gasoline spikes. When gasoline spikes, the cost of transporting consumer goods—from fresh produce to electronics—increases. Retailers refuse to absorb those elevated shipping costs, so they pass them directly onto you at the register.

If you are looking for strategies to offset rising utility bills and transportation costs, you are not alone. The macro-economic data is translating into a micro-economic crisis for households trying to balance stagnant real wages against soaring energy prices.

The “Core CPI” Illusion: Why the Federal Reserve’s Math Feels Wrong

Here is where the disconnect between the government and the citizen happens. When you turn on financial news networks, you will hear pundits talking endlessly about “Core CPI.”

The core inflation figure for March 2026 came in lower than the headline number, hovering around 2.6%. The Federal Reserve strongly prefers to base its monetary policy on this core metric.

Understanding the Difference Between Headline Inflation and Core Consumer Prices

To calculate Core CPI, economists take the standard inflation data and completely strip out food and energy costs. Their reasoning is that food and energy markets are highly volatile and subject to sudden global shocks (like a bad harvest or an overseas conflict). They believe core data gives a better picture of underlying, long-term economic trends.

From an academic standpoint, that logic holds up. From a human standpoint, it feels like pure economic gaslighting.

We buy food. We buy gas. These are not optional, discretionary expenditures. They are the absolute foundation of our daily survival. When the Federal Reserve points to a cooling “core” inflation rate while you are simultaneously paying 15% more to fill your tank and feed your family, the disconnect breeds intense frustration. The average consumer does not live in a “core” economy. We live in the headline economy. And right now, the headline economy is bleeding our disposable income dry.

Will an Interest-Rate Cut Happen in 2026?

For months, the narrative from central banks—both the Federal Reserve in the US and the Bank of England in the UK—was cautiously optimistic. The expectation was that we would see three, perhaps four, interest-rate cuts throughout 2026. Those cuts were supposed to be the cavalry coming over the hill to rescue households drowning in high-interest debt.

Why the March Inflation Jump Is Keeping Borrowing Costs Painfully High

You can safely assume the cavalry has been delayed indefinitely.

The Federal Open Market Committee (FOMC) has a strict mandate: achieve a target inflation rate of 2%. With the March CPI data showing a reversal back up to 3.3%, the Fed’s hands are essentially tied. Cutting rates injects liquidity into the economy; it makes borrowing cheaper, which spurs spending. If the Fed cuts rates now, while energy-driven consumer prices are already surging, they risk pouring gasoline on a newly reignited inflationary fire.

As a result, we expect a “higher for longer” monetary environment. The immediate ramifications for your wallet are severe:

- Mortgage Rates: If you were waiting to buy a home or refinance an existing loan, the cost of borrowing will remain prohibitively high. Understanding how the Federal Reserve impacts your mortgage is crucial; even minor delays in rate cuts translate to tens of thousands of dollars in interest over the life of a loan.

- Credit Cards: Annual Percentage Rates (APRs) on credit cards are sitting at historic highs. With no rate cuts on the horizon, carrying a month-to-month balance is more toxic to your wealth than it has been in two decades.

- Auto Loans: Financing a new or used vehicle will continue to carry a massive interest penalty, further complicating the lives of commuters already struggling with high gas prices.

The central banks are trapped. They cannot lower rates to stimulate growth without risking hyper-inflation, and they cannot raise them further without risking a severe recession. We are stuck in a holding pattern, and the consumer is bearing the weight of the stagnation.

Navigating the Surge: How to Protect Your Purchasing Power This Spring

Knowing why your wallet is emptying faster is only half the battle. The other half is playing aggressive financial defense. Since macroeconomic forces and central bank policies are out of our control, we must hyper-focus on what we can control at the household level.

1. Audit Your Energy Consumption Because energy costs are the primary driver of the March 2026 CPI jump, you have to ruthlessly audit your usage. Consolidate your driving trips. If you have a hybrid work schedule, maximize your work-from-home days to avoid the gas pump. Look into local government subsidies for home insulation or smart thermostats to curb heating and cooling leakage.

2. Attack Variable-Rate Debt With interest-rate cuts off the table for the immediate future, any variable-rate debt you hold is a financial emergency. Prioritize paying down high-interest credit cards before funneling money into standard savings accounts. A savings account yielding 4% cannot outpace a credit card charging 24%.

3. Combat the Grocery Aisle Squeeze Food prices, while excluded from the core inflation data, are still a massive pain point. Brands are aggressively reducing package sizes while keeping prices identical. We highly recommend educating yourself on fighting grocery shrinkflation by checking unit prices (cost per ounce or gram) rather than the sticker price, and heavily leaning into generic store brands for pantry staples.

The US core inflation March 2026 data is a harsh wake-up call. The era of cheap money and predictable prices has not returned. By understanding the mechanics of energy costs, the reality of CPI data, and the Federal Reserve’s hesitation, you can strip away the confusion and make informed, defensive moves to protect your family’s financial future.

ViralZip.blog is powered by a dedicated team of digital analysts and tech journalists committed to “zipping” through the noise of the information age. With a combined background in investigative research and financial data analysis, our contributors focus on the intersection of emerging AI technology, local economic shifts, and global news trends. We take pride in translating complex data into actionable insights for modern residents across the US and UK. Our mission is to provide high-velocity, reliable information that empowers our readers to navigate the rapidly evolving landscape of 2026.

Disclaimer: The content provided on ViralZip.blog is for informational and educational purposes only. While we strive for accuracy, the fields of artificial intelligence, financial rebates, and medical technology are subject to rapid changes; therefore, we do not guarantee the completeness or absolute reliability of the information provided. This content does not constitute professional financial, medical, or legal advice. Always consult with a licensed professional—such as a financial advisor, doctor, or attorney—before making significant decisions based on trending data. ViralZip.blog is not responsible for any actions taken or outcomes achieved based on the suggestions provided in our articles.